Resources for Credit Unions and their directors, lenders and associations

Here are the follow-up resources for presentations for Credit Union Leagues and professional associations and articles in Credit Union magazines. I have combined them for a complete resource for you.

Quicklinks by client

June 2011 NW Credit Union Association Volunteer’s Conference

August 2010 Quickbites Teleseminar (Listed on websites of 18 CU Associations)

December 2009 CUES Webinar

November 2009 CUNA Lending Council Conference

Quicklinks by content

Presentations:

Finance 2.0 for CU Directors

Slideshow PPT

More Trouble Brewing: Are your Guidelines Getting in the Way of Saying ‘Yes’ to Self-employed Members?

Handouts

Recap of session

Recommended Guidelines

Responsibilities of CU Directors in the New Normal

Ten Essentials List

Self-Employed Members in Rough Waters: How to Say Yes

Slideshow

Handouts

Resources:

Complimentary eCourse on Tax Return Analysis for your Lenders

CU Directors Online Training

Guideline Recommendations for Lending to Self-Employed Members

Lender ‘Knowledge Check’ on Tax Return Analysis

Loan Request Guidelines (Customizable)

Site-wide Search of this website

Subscription to ‘Lender Asks’ ezine

Discount on Loan Analysis and ALLL software

June 2011 NW CU Association Volunteer’s Conference:

Finance 2.0 for CU Directors: Move from Check-the-Box to Good Governance

Download the PDF of Slide Show

Responsibilities of CU Directors in the ‘New Normal’

The Essentials of Success for CU Directors and Volunteers

Attendees added to the following ideas from Volunteers at numerous Credit Union Association conferences. In some cases I have put the same ‘essential’ is in two categories.

Would you like to add an ‘Essential’? Email me at Linda@LindaKeithCPA.com and I’ll put it on the list!

Understand the Role of the Board and of Directors

- Have a questioning attitude…no rubber stamp

- Understand ‘Good Governance’

- Speak up – don’t be afraid to ask questions

- Take time to adequately prepare before meetings

- Obtain basic financial literacy

- Study the basic governance structure and understand it well

- Value and appreciate differences of opinion

- Be willing to learn anything and everything you need to know

- Remember you represent all the membership

- Know your job

- Practice critical listening along with self censoring of tasks or inquiries

- Train and find your successor

- Don’t micromanage—Details about CU are for CEO.

- Ask key question w/o being confrontational

- Do not be overwhelmed by info

- Know when no opinion is okay

- Understand the difference between policy/strategy and procedures/tactics

- Learn how to stay out of the weeds – strategic direction: what does it mean

- Have broader than just a finance background

- Take responsibility for recruitment and retention

- Cultivate the ability to see the world from 30,000 feet

Traits

- Questioning attitude

- Willingness to ask questions

- Comfortable with differences of opinion

- Listens carefully and critically

- Self censors as needed

- Good ‘bullshit’ meter

- Curious

- Flexible

- Positive attitude for forward progress

- Observant

- Committed to the CU and members

- Not easily overwhelmed

- Willing to express no opinion if you have none

- Clear Communicator

- Open mind

- Humility – you don’t know it all

- Competent

- Patient

- Willing to engage in ongoing director dialogue

- Creative thinker

- Assertive

- Ability to see the world from 30,000 feet–avoid micromanagement

Relationships

- Open, trusting relationship with CEO

- Always be kind to others (both volunteers and mgmt)

- Mentoring by experienced director

- Ask key question w/o being confrontational

- Importance of ongoing director dialogue

- How to talk to members when asked questions

- Board and Management interaction

Willing to

- Attend meetings

- Block out sufficient time to adequately prepare for board meetings

- Read and understand board packet info before the board meeting

- Learn CU Finance at a Director level

- Study the basic governance structure and understand it well

- Learn anything and everything you need to know

- Obtain continuing education

- Find and train your successor

- Conscious decision to seek out a variety of viewpoints

CU Finance

- Obtain or increase basic financial literacy

- Interpretation of trends…what are peer groups?

- What are the indicators by importance?

- How to read budget sheet

- How to use CU financil reports for policy-making and strategic planning

- Confidence in knowing financials

- Basic business and financial experience

- Specific ratios: Capital to Asset, Operating Expense, Net Charge Offs and Delinquency Ratio

Specific Skills/Knowledge

- How to choose/manage a CEO

- How to plan strategically

- Have a documented governance model and rely on it as a framework

- Public relations experience

- Legal background

- Communicate well

- Ability to see the world from 30,000 feet

- Basic business and financial experience

August 2010 Credit Union Association Teleseminar:

Lending to the Self-Employed: How to Say “YES”!

December 2009 CUES Webinar

More Trouble Brewing:

Are your Guidelines Getting in the Way of Saying ‘Yes’ to Self-Employed Members?

Download PDF of Handouts (6 pages of 6 slides per sheet ~ smaller print)

Download PDF of Handouts (18 pages of 2 slides per sheet ~ larger print)

Recap of session

All agreed that Credit Unions have two strong incentives to improve their ability to say ‘yes’ to self-employed members:

- As member-owned organizations, there is a moral obligation to lend to our self-employed members if they qualify. There is also a moral obligation to protect the assets of the credit union (and thus serve all the other members) by better understanding when a loan or restructure should be declined.

- There is an opportunity as some community banks retrench to capture more of the small business marketplace, especially if the credit union also offers Member Business Loans (MBL).

My Guideline Recommendations for Self-Employed Members

The notes below each one are modifications suggested by the attendees…

- Use three year’s tax returns

- Update guidelines and communicate them clearly

- Include YTD Financial Statement in averages when appropriate

- If using YTD Financial Statements, require CPA-prepared

- Select subject matter experts for advanced training and resources

Attendees suggestion:

Some CUs (based on size) thought this would be going too far.

Attendees suggestions:

Do not request the financial statements if you are sure you will decline the loan (due to cost to the member).

Add requirement for supporting documents such as bank statements, etc. (Yes, the CU lender did say ‘bank’.)

Clarified that the personal as well as business financial statements must be obtained.

Reconcile financial statements with tax returns. (Discussed differences due to cash vs accrual, etc.)

Attendees suggestions:

Training needs to be quarterly or semi-annual. Not just once-and-done.

For a sole proprietorship, make a list of seasonal work, incorporate lean months etc. to explain seasonality

Know your members. If long term and lots of products per member, don’t require they jump through all the hoops. (We discussed consistency issues and requirement that policy or procedures be clear to avoid inadvertent discrimination.)

If the member’s business is not a sole proprietorship, obtain and review the articles of incorporation or partnership/llc agreement. Determine number of owners and learn more about the business.

Attendee Guideline Recommendations

At the conference session, the Chief Lending Officers in attendance spent time in small groups to discuss which guidelines made sense for their Credit Unions, their markets, and the type of loans they make to self-employed members. These additional suggestions came out of the small groups:

- Be sure to look at the entire relationship, not just the financials.

- If your credit union is too small to gear up for this, consider hiring third parties to do the analysis. (There was discussion about how to find them.)

- As a member benefit, consider training for self-employed members about financial statements (preparation and/or analysis for management purposes).

- Review the member’s website as another way to better understand their business.

- If the member has a lot of rental properties, get the rent roles. Compare to tax returns to see if properties are consistently rented.

- Make decisions about when we may not need full tax returns. For example, high credit score or low loan-to-value.

- Align procedures so that requirements match the complexity and/or amount of the loan.

- In policy require ‘verification of income’. In procedures spell out what that means regarding different criteria such as number of years membership, credit score, loan-to-value, etc.

- Spend more time with lenders understanding some of the standard adjustments, like depreciation.

November 2009 CUNA Lending Council Conference

Self-employed Members in Rough Waters:

How to say YES

Resources

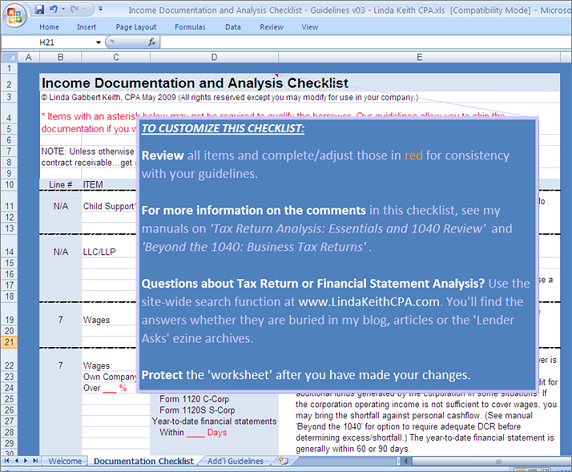

Customizable Income Documentation Worksheet

Info@LindaKeithCPA.com and request your complimentary copy.

Info@LindaKeithCPA.com and request your complimentary copy.

We will send it to you and schedule the phone consultation to customize it to your guidelines. It will give you and me a chance to discuss any guideline changes you might want to consider.

Once it is done, we password-protect and get it out on your network. Now all the lenders, the underwriters, even the regulators can see the consistent, recently updated guidelines. And the lenders will know what to do with each type of income.

Discount on Analysis and ALLL software:

I have a strategic partnership with Sageworks Inc, a leading provider of loan and portfolio analysis software. They have recently launched a new component called ‘Surety’ which handles ALLL calculations and reports incredibly well.

Full Disclosure: I have a business relationship with their company. The good news is, because of that relationship I am able to offer a 15% discount to my referrals. .

So check them out at their website. And if you are interested, email their Director of Business Development, Cathy Moore, directly to get the discount.

Free resources for you and your lenders:

1) A ‘knowledge check’ on tax return analysis. A senior lender should take it first to determine if the level is appropriate for your lenders.

2) A free eCourse Intro to Tax Return Analysis

From our www.LendersOnlineTraining.com site, this is one of the complimentary eCourses and will help your lenders

- Understand the big picture and feel more comfortable with tax returns

- Get a feel for what they are looking for

- Learn a process to save time and insure they have all the pages they need

Click here to access the eCourse.

3) Complimentary subscription to ‘Lender Asks’ eZine

The best way to learn tax return analysis is incrementally. One answer to one question posed by a lender on tax return or financial statement analysis is featured each month.

Each issue includes the list of all the blog posts during the month at ‘Good Loans. More Loans.’ and they can click right through to the one that interests them.

Click here to sign up for our ezine.

4) Use our site-wide search or ask Linda when questions arise

When a lender has a question about tax return or financial statement analysis, it is very likely I have already answered it.

In the lower left corner of every single page in this website there is a site-wide search box. Put in your search term and you’ll find the answer whether it is buried in articles, blog posts or the ‘Ask Linda’ archives.

If the answer is not there, click on the ‘Ask Linda‘ page and ask. It is truly that simple.

[back to top]

Credit Union Director’s Online Training

I have started a ‘Director’s List’ which I’ll use for periodic emails when something comes out that I think is of interest. This is not currently slated for even monthly use and the email addresses will never be shared with anyone.

The project that is in the works and will be announced to this list is ‘Director’s Online Training’. Actually, it will be helpful to Directors, Supervisory Committee Members and even to mid-level management. The focus for now is Finance.

Sign up here to get on the list. You can opt back out whenever you choose.

Other resources to consider…

I help lenders say ‘yes’ to good loans. Here are a few ways that I can help you further.

Training for your lenders

- Bring me in-house to train to your guidelines, your type of lending, your lenders’ experience level

- Send your subject-matter experts to my open-enrollment workshops

- Subscribe individual lenders or your whole lending team at www.LendersOnlineTraining.com for 20 eCourses covering tax return analysis for loans to self-employed members or to businesses

- Between you and other area credit unions, commit to five paid attendees and provide a meeting room and we’ll schedule a ‘local’ program in your area, anywhere in the United States

Print and electronic resources

- Purchase manuals on tax return and financial statement analysis for your lenders, or your subject matter experts, or for each branch.

- Purchase my Global Cashflow Worksheet to customize your tax return analysis process. I’ll customize them to your guidelines first.

Call me and let’s talk.

I keep my finger on the pulse of lending and regulating by talking to people just like you every week. I am a real fan of ‘NOW’ and ‘NEXT’, understanding where we are and figuring out the best steps forward. We’ll both enjoy the conversation and I’ll bet we both benefit from it, as well.

How else can I help you?